How to set realistic financial goals when creating a budget

How to set realistic financial goals when creating a budget

Setting realistic financial goals is a critical pillar of effective personal finance management. This process, often encapsulated in 'budget planning', empowers you to gain control over your financial future. An engaging budgeting journey involves not only the mechanics of calculating 'income' and 'expenses' but also the art of setting achievable 'financial goals'. In this article, we'll delve into how to shape these objectives, making budgeting a less daunting task and a more effective tool for fulfilling your financial dreams. With these insights, 'realistic budgeting' and 'financial stability' can become your newfound forte.

Know Where You Stand: Assessing Your Finances for Realistic Budgeting

- Conduct a financial assessment to understand income, expenses, and status.

- Evaluate the budget by looking at spending habits.

- Figure out ways to cut costs and set goals.

- Study debt and savings to see their effect on the budget.

- This will help make decisions for managing finances.

Unexpected expenses and future goals are crucial for a budget that fits your financial situation. As a result of taking these factors into account, you can create a budget to reach long-term goals.

Identify Your Financial Priorities: Defining Goals and Needs

When defining goals and needs, recognizing your financial priorities is key. It helps you grasp what is significant to you and make your budget fit those priorities. Figure out what matters to you financially and you can concentrate on the vital parts and share resources suitably. Here are some steps to effectively recognize and define financial priorities:

- Look at Your Values: Ponder what is important money-wise to you. This could include safety, autonomy, or a well-off retirement.

- Assess Your Status: Consider your current finances, such as income, outgoings, debts, and savings. Knowing your current financial spot will help set achievable goals.

- Set SMART Targets: Be sure your goals are Specific, Measurable, Achievable, Relevant, and Time-bound. Instead of saying, "I want to save more money," set a specific target, such as "I want to save $500 a month for the next six months."

- Rank your goals: You should rank them according to their urgency or effect on your other responsibilities. Make sure you take into account both the short-term requirements and the long-term goals.

- Create a Budget: Create a precise budget that reflects your financial priorities and helps you reach goals. Give resources according to their importance as found in past steps.

- Review and Change Frequently: Regularly check your progress towards achieving financial goals and change as appropriate. Situations vary over time, so it is essential to make regular changes that show new priorities or unforeseen events.

These steps can help you make a practical budget that fits your needs and achieves meaningful results. Setting targets and allocating resources according to your personal preferences is essential because everyone's financial situation is unique.

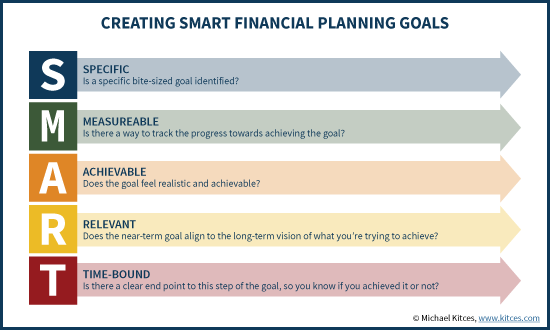

SMART Goal Setting: Creating a Blueprint for Financial Success

- Identify your objectives: Figure out what you want to achieve monetarily, such as paying off debt, saving for retirement, or buying a house.

- Make goals specific: Don't just say "save money," decide how much and by when. This helps with planning and tracking progress.

- Ensure goals are measurable: Break 'em down into smaller, measurable targets or milestones. This keeps you motivated and allows you to track your progress.

- Achieveability: See if the goals are realistic and possible within your means. Adjust if needed.

- Relevance: Check that your goals connect to your financial desires and values. Rethink if not.

- Time-bound objectives: Set deadlines to stay accountable and prevent procrastination. A timeline adds structure and urgency.

- Be flexible: Regularly review and adjust your goals as needed. Financial success needs adaptability and endurance.

From Vision to Achievement: Breaking Down Long-Term Goals into Milestones

Transform long-term financial objectives into actionable achievements by breaking your goals into smaller milestones. Here's a guide that helps:

- Define your vision. Start with a clear, long-term financial goal. It could be saving for retirement, buying a house, or starting a biz.

- Set specific milestones. Break your goal into smaller, achievable parts. These could be time-based or monetary targets to track progress and stay motivated.

- Create an action plan. Know the steps needed to reach each milestone. Assess your finances, set a budget, cut expenses, increase income, or invest.

- Track your progress. Monitor and assess your progress against each milestone. Use financial tools/apps to make tracking easier.

- Adjust and celebrate. As you make progress to each milestone, adjust your plan if necessary. Celebrate each achievement to stay motivated!

Breaking down objectives into actionable milestones, tracking progress, and customizing your approach per your circumstances and aspirations will increase your chances of success and achieving your financial goals!

Budgeting with Reality: Being Realistic about Income and Expenses

A realistic approach to our finances is crucial. A vital part of successful budgeting is creating achievable financial goals based on our current financial situation. We can create a reasonable budget by accurately assessing our income and expenses.

First, we need to evaluate our income sources. This includes salary, freelance work, and investment returns. We must be realistic about how much we can expect to earn regularly. By considering potential fluctuations, we can make better budgeting decisions.

We also need to acknowledge our expenses. Fixed expenses like rent, utilities, and insurance must be accounted for, as well as varying expenses like groceries, transportation, and entertainment. Knowing the exact amounts spent in each category helps us allocate funds correctly.

It is important to consider irregular expenses that may occur during the year. These include medical emergencies, car repairs, and home maintenance costs. Setting aside a buffer for such expenses allows us to remain financially stable even during unpredictable times.

In a nutshell, realistic budgeting involves an honest assessment of our income and expenses. It allows us to set achievable financial goals, accounting for potential fluctuations and unforeseen circumstances. With this approach to budgeting, we can ensure our financial well-being and future security.

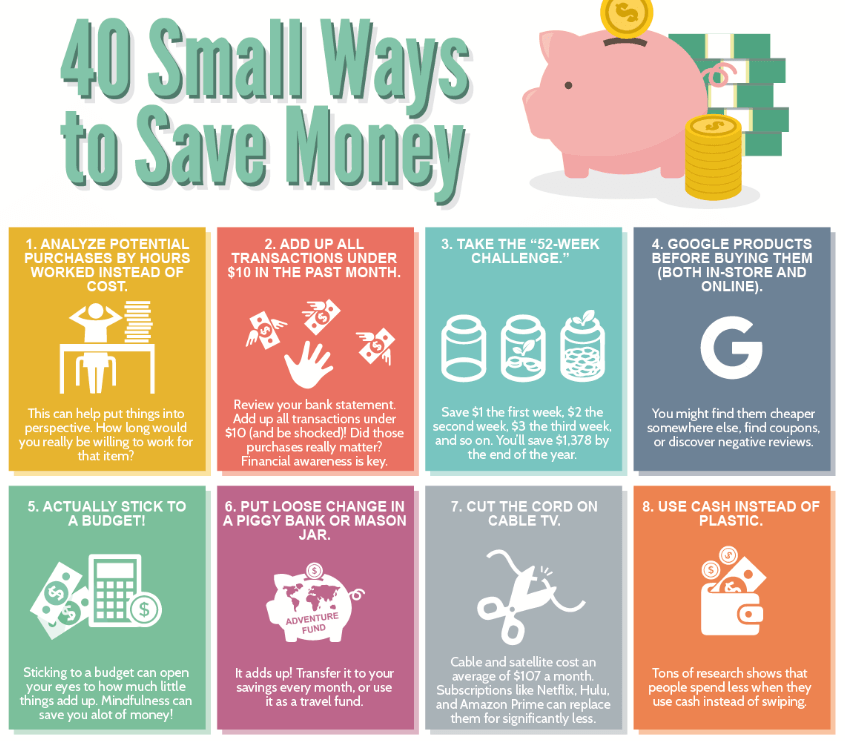

Credit: https://www.titlemax.com/discovery-center/lifestyle/40-small-ways-to-save-money/

Trimming the Excess: Adapting Your Lifestyle for Financial Goals

For financial success, it's important to reduce unnecessary expenses.

- Figure Out Spending Habits: Take a closer look at expenses. See which ones are necessary and which can be cut.

- Create a Realistic Budget: Set financial goals and make a budget to match them. Allocate funds for needs, savings, and debt repayment. Also, plan for unexpected expenses.

- Cut Back on Discretionary Spending: Find areas where you can reduce spending without affecting life quality. This can include less eating out, canceling unused subscriptions, and finding more cost-effective alternatives.

- Save on Essentials: Look for opportunities to save on essential expenses like groceries, utilities, and transport. Buying in bulk, energy-saving strategies, and public transport options can help.

- Get Support and Accountability: Tell friends or family your goals and ask for support and accountability. Join online communities or get guidance from financial advisors to stay motivated.

By making these lifestyle changes and sticking to a budget, financial success is possible and still enjoy the present without overspending.

Keeping Pace with Progress: Regularly Reviewing and Revising Your Financial Goals

The key to success is continually assessing and altering your goals. Routinely review them to get an accurate grasp of your situation and make the necessary adjustments.

This helps you stay focused and motivated, adapting your plans based on changing conditions or new opportunities. It also keeps your objectives relevant, realistic, and aligned with your long-term goals.

- Tracking Progress: Regular goal review is vital for successful financial planning. Track your progress against the benchmarks to spot any gaps or issues between where you are now and where you want to be. Plus, it ensures you take advantage of new trends and alter strategies when needed. Keeping tabs on your goals lets you work towards improving your finances continuously.

- Adaptability: Frequent assessment allows for adaptability. Financial markets, personal situations, and unexpected events require different approaches. Evaluating regularly identifies potential risks or areas where you need to make changes.

- Strategies for Regular Goal Review: To keep up with progress through regular review, use efficient strategies such as setting specific timeframes for evaluation. Have a routine for assessing each objective. Utilize tech tools or work with a trusted advisor for advice. Analyze your performance against targets regularly.

Also, set milestones or sub-goals to break down significant objectives into smaller ones. Doing this create an informed financial plan that will adjust to your changing circumstances and maximize success.

Staying Motivated: Celebrating Milestones on Your Financial Journey

Recognize and reward yourself for reaching financial goals. Set small, achievable objectives so you can follow your progress. Treat yourself to something special within a budget when each milestone is reached.

Share your successes with family and friends, forming a support system to boost motivation. Ponder how much you've achieved and the positive effect your milestones have had on your financial wellbeing.

When celebrating, use it as a chance to set new goals and carry on towards financial success.

Remember this during your financial voyage for ongoing motivation and cheer. Additionally, staying motivated aids focus and discipline, avoiding exhaustion. Aiming towards landmarks and celebrating accomplishments not only improves your financial health but also serves as encouragement for others on their own financial paths.

To sum up

In conclusion, setting realistic financial goals is indispensable to creating a budget. This process entails clear identification of all income sources and accurately tracking your expenses. You can pave the path toward a secure financial future by designing a comprehensive budget plan, applying strategic rules, and regularly reviewing and adjusting your budget. Incorporating an emergency fund and prioritizing debt elimination further enhance your budgeting strategy. Remember, the essence of 'financial management' lies in effectively aligning your 'personal finance' and 'budgeting' goals. Your journey toward financial freedom begins with a realistic budget grounded on well-set financial objectives. This proactive approach can transform your 'savings', 'income', and 'expenses' into tools for achieving your financial dreams.