How to Create a Budget for a Family or Household

Financial instability is a mounting issue for families and households worldwide. Fortunately, however, these individuals don't have to grapple with monetary unpredictability once they know how to craft a fitting budget. That's what you'll learn about in this article. Understanding how to create a budget for a family or household serves as a robust shield against unexpected expenditures, ensuring financial security and peace of mind. With practical budgeting strategies in place, a path to financial health becomes much clearer. Dive into this article to learn effective methods to handle your household's finances.

1. Prioritizing Essential Expenses for a Balanced Household Budget

- Identify and sort must-have costs, like rent or mortgage payments, utilities, groceries, and healthcare.

- Check out discretionary spending and non-essential items to ensure the money is allocated towards vital needs.

- Change the budget regularly based on changing conditions or financial objectives to keep a well-balanced approach for essential family expenditures.

When forming a family budget, it's crucial to prioritize essential expenses while looking at household income and expenditure trends. Families can guarantee that their funds align with their most critical needs by categorizing necessary costs and evaluating discretionary spending. By doing this, they can create a fair household budget that supports their general financial health and stability.

2. Engaging Your Family in Household Budgeting

- Make budgeting a team effort and its importance clear.

- Schedule family meetings to talk about financial goals and how far you've come.

- Teach family members budgeting basics: tracking expenses and setting spending limits.

- Welcome ideas from everyone to save money and avoid unnecessary costs.

- Put everyone in charge of their own spending records.

- Celebrate successes as a family when financial targets are achieved or surpassed.

Getting the whole family onboard with managing finances requires creative strategies. Helping everyone be part of the process through sharing goals and assigning tasks makes sure everyone feels invested.

3. Setting Clearly Defined Financial Goals for Your Family Budget

Want to make a family budget? Establish realistic financial objectives by following these three steps.

- Evaluate current finances: Begin by looking at your family's income, expenses, and debts. This will help you see where improvements can be made and how much you can save or use for debt payment. Analyze your spending habits and pinpoint unnecessary costs.

- Define long-term goals: Now, set up long-term goals for your family. These can be saving for children's education, buying a house, or planning retirement. Put them in order of importance and make a timeline for achieving them. Make sure they're specific, measurable, achievable, relevant, and time-bound (SMART).

- Set short-term milestones: To stay motivated and monitor progress, set smaller goals that can be achieved in weeks or months. For example, if your long-term goal is to save for a house in five years, set monthly savings targets.

By setting realistic financial goals in this way and regularly checking up on them, you can make informed decisions and maintain financial stability for your family. Keeping objectives SMART avoids overwhelming expectations or circumstances.

Credit: https://www.pewresearch.org/social-trends/2007/02/07/what-americans-pay-for-and-how/

4. How to Track and Control Household Expenses

Keep tabs on and control your household costs for financial security. Here's the lowdown on how to monitor and regulate your spending - ensuring a secure financial future for all.

- Make a full list of your regular expenses. Include fixed costs (like rent/mortgage, utilities) and variable ones (like groceries, entertainment).

- Use expense-tracking tools or budgeting apps to log your spending. They can help you spot areas you can reduce and save money.

- Assess your monthly income and allocate budgets to different expense categories. This allows you to focus on essential needs and cut back on costs.

- Review your progress often and make necessary changes. Pay attention to your spending patterns to control your household expenses.

Doing this allows you to manage and monitor your household expenses efficiently, setting yourself and your family up for long-term financial stability. Remember: heaps of expense-tracking tools and budgeting apps are available to aid you in the process.

5. Strategies for Saving in Your Family Budget

- Allocate a fixed percentage of your income to savings each month.

- Cut back on non-essential expenses.

- Analyze monthly expenditures and find areas to reduce spending.

- Establish clear financial goals for your family.

- Utilize technology to track and manage your budget.

- Involve the whole family in the budgeting process.

- Teach children about money management.

- Incorporate creative ways to save money without sacrificing quality of life.

- Implement effective strategies into your family budget to prioritize savings and meet financial obligations.

6. Minimizing Discretionary Expenses in Your Household Budget

- Spot non-essential costs. Look into your buying habits and pick out what's not essential for your family's wellbeing.

- Set limits on spending. Make realistic budgets for luxury items, such as entertainment or eating out, to dodge overspending.

- Save more than expend. Put aside a portion of your income for savings before allocating money for discretionary spending.

- Follow frugal living. Adopt more simple and affordable alternatives in your daily life to cut down on unnecessary expenses.

- Monitor expenses often. Track your discretionary spending often to see where you can save more money.

- Plus, bulk buying and using coupons can help you minimize discretionary spending without sacrificing quality or comfort in your budget.

7. Budgeting for Irregular Expenses in Your Family Financial Plan

- Prioritize savings for sudden costs, like car fixes or medical bills.

- Make a distinct category in your budget for irregular expenses, assigning a specific amount every month.

- Figure out the average you spend yearly on irregular expenses and use that to decide how much to store away each month.

- Modify your budget if needed based on changes in your situation or financial objectives.

Planning and budgeting in advance can help evade debt and financial pressure when irregular expenses arise.

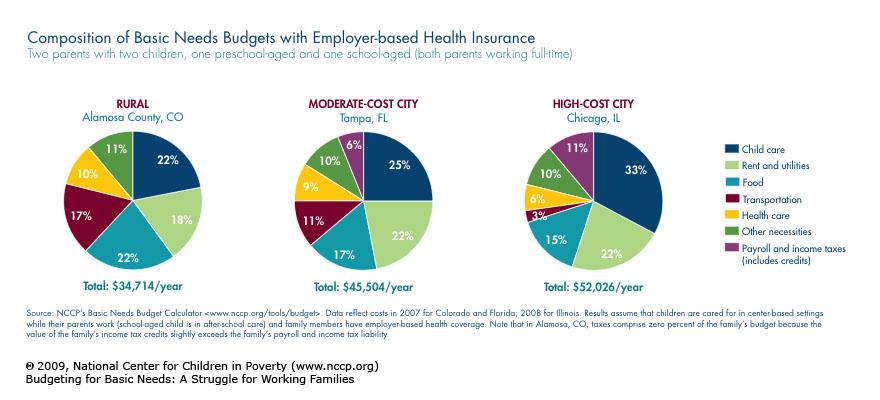

Credit: https://www.nccp.org/publication/budgeting-for-basic-needs-a-struggle-for-working-families/

8. Budgeting for Education and Childcare Expenses

Financial preparation for schooling and childcare is essential for family stability. Here are some points to remember:

- Checking Education Costs: Consider tuition, supplies, uniforms, activities, and transport.

- Calculating Childcare Expenses: Consider babysitters, daycare, after-school, and summer camps.

- Examining the Budget: Look at your budget regularly. Check if it's suitable for educational and childcare needs. Make changes when needed.

- Financial Security: Make a back-up plan. Put aside money for unforeseen educational or childcare expenses.

Get a budget that fits in with potential changes in educational costs and childcare requirements. You should make regular adjustments to your budget. By doing this, you can provide your children with quality education and care while also ensuring financial security.

The Importance of Family Budgets

A family budget plays a vital role in securing financial health. It's the financial blueprint that helps balance income and expenses, ensuring you're not spending more than you're earning. With a well-planned budget, families can prioritize spending, steering resources toward needs over wants. It aids in setting aside funds for emergencies and fulfilling long-term financial goals like buying a home or planning for retirement. A family budget encourages disciplined spending, fosters healthy financial habits, and teaches kids about money management.

Furthermore, it provides a sense of control over your money, reducing financial stress. A family budget contributes to a more peaceful home environment by making finances predictable. Remember, a family budget isn't about restriction. It's about making money work best for you. It's the compass guiding your financial journey, facilitating stability and security for a prosperous future. So, start budgeting and experience the financial freedom it offers!

Which budget rule is the best

Choosing the "best" budget rule is like picking the right tool for a job - it depends on the specific financial situation and objectives. Popular rules like the 50/20/30 rule or Zero-Based budgeting offer unique benefits. The 50/20/30 rule is excellent for people who prefer simplicity, allocating 50% of income to needs, 20% to savings, and 30% to wants. On the other hand, Zero-Based budgeting is for those who value precision, where every dollar has a specific purpose.

Other options include the Envelope system, an excellent choice for those trying to curb overspending, or the Values-based budget, appealing to those prioritizing spending in areas they care about most. Evaluating the "best" budget rule requires understanding financial goals, discipline, and lifestyle. It's not a one-size-fits-all answer but a personalized approach to managing finances effectively.