Do you need a loan to buy a car?

Buying a car is an exciting and necessary purchase for many. Yet, depending on the model and make of the car you want, it can come with a hefty price tag. A loan to help cover the cost may be one way to finance your purchase. But why might someone decide to use this type of financing?

In this article, we will provide a brief overview of why people opt for loans when buying cars.

Benefits of a car loan

One reason why taking out a loan may be beneficial is that it allows you to pay off larger items over time instead of needing the full amount up front. It also helps spread out payments over several months or years to make them more affordable for your budget. Additionally, by taking out a loan for your car purchase, you can start building credit if you don't already have an established credit history.

Downsides of a car loan

Purchasing a car is a significant financial decision and requires careful consideration of the different types of loans available. Understanding the various loan options can help car buyers make an informed choice and get the best deal possible.

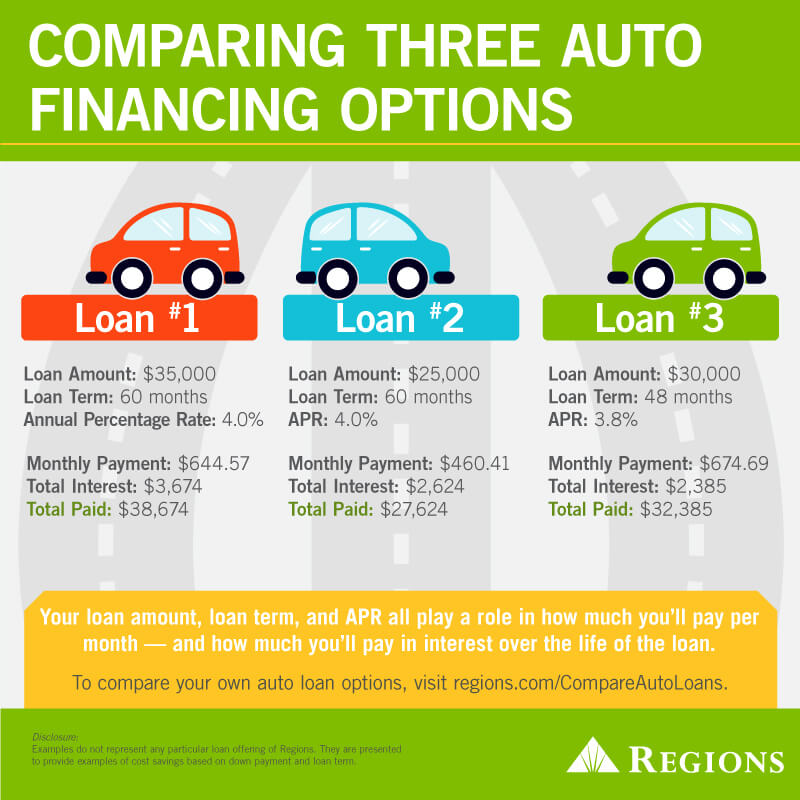

When it comes to financing your vehicle purchase, there are several loan types that you should be aware of. For starters, banks, credit unions, and other lending institutions offer traditional auto loans at competitive rates. These are typically secured loans requiring borrowers' good credit scores to obtain favorable terms. Additionally, some dealerships may offer their financing plans with more flexible terms than those available from banks or credit unions, though these tend to have higher interest rates.Although loans can offer financial assistance with the vehicle's purchase, they come with certain risks and should be carefully weighed before committing. Interest rates are one of the most consequential drawbacks when taking out a loan for a car. The interest rate will affect how much money you pay each month and, over time, potentially lead to considerable long-term financial commitments if not appropriately managed. Other fees may also be included in your monthly payment, such as late charges or prepayment penalties which could further cause an increase in your debt load.

Credit: regions.com

Alternative financing options

When you're looking to purchase a car, there are a variety of ways to finance the purchase. Alternative financing options such as cash purchases, leasing, and personal loans can be as viable as taking out an auto loan from a bank or other financial institution.

Cash purchases are often the most straightforward way of purchasing a car since the buyer is responsible for covering the total cost upfront. However, some buyers may not have the funds available to pay for a vehicle in full right away. Leasing is an attractive option because it provides an opportunity to drive a more expensive or newer model than what they could typically afford with lower monthly payments than if they were to take out an auto loan. Personal loans may also be used when buying a car and offer competitive interest rates and loan terms depending on creditworthiness.

How to apply for a car loan

Applying for a car loan can be intimidating, especially when there are so many factors to consider – from gathering the necessary documents to comparing loan offers and evaluating credit scores. But with a few simple steps, applying for a car loan can be easy and stress-free.The first step in applying for a car loan is gathering all the paperwork, such as proof of identity, residence, income statements, and bank statements. Once you have these documents on hand, you can compare offers from different lenders and evaluate your credit score to determine which terms best suit your needs. When looking at each lender's proposal, it's essential to pay particular attention to the interest rate offered, as this will significantly affect your monthly payments.

Credit: 3riversfcu.org

Conclusion

Financial decisions are some of the most critical choices we make in life. Deciding to take out a car loan is no exception. There are several vital points when considering if a loan is a right choice for you.

When deciding whether or not to take out a car loan, a critical point is your financial situation and credit score. Your financial status must allow you to repay the loan on time and in full each month. Otherwise, you may be charged late fees or higher interest rates due to missed payments. Additionally, having an ideal credit score will help qualify you for lower interest rate loans as well as open up more options from lenders. Another point to consider when taking out a car loan is the total cost of ownership.

In today's economic climate, it is more important than ever to carefully evaluate your financial situation and explore all options before making any decisions. To determine if taking out a loan is the best option for you, it is essential to review your income and expenses and investigate the different types of loans available to determine if taking out a loan is the best option for you.

Before signing any loan documents, there are several questions that you should ask yourself. How much can I afford? Does the loan come with any additional fees? What type of terms do I agree to? Will I be able to make the payments on time? Answering these questions will help you better understand what kind of loan will work best for your circumstances.