Budgeting for Retirement: Planning for the Future

Budgeting for Retirement: Planning for the Future

Navigating the path to retirement can be an exciting yet daunting journey. It's about more than just stopping work - it's about creating a financially secure future that aligns with your lifestyle aspirations. Successful 'budgeting for retirement' forms the crux of this process, ensuring you have the means to live your desired post-retirement life. Each step plays a crucial role, from understanding your retirement goals to managing your income streams, outlining post-retirement expenses, planning for healthcare costs, managing debts, and maximizing savings and investments. Regular reviews and adjustments further refine your retirement budgeting strategy. This comprehensive guide will delve into these points, helping you navigate the retirement planning process with confidence and foresight. Let's begin the journey of securing your golden years.

Assess Your Retirement Lifestyle Goals

Planning for your golden years starts with a vision. What does your ideal retirement look like? Do you see yourself lounging on a beach, transforming your hobby into a small business, or dedicating more time to family? Picturing this can clarify your retirement lifestyle goals and shape your 'budgeting for retirement' strategy.

It's not just about having enough to get by; you want a comfortable life that allows you to engage in desired activities and pursuits. This vision helps estimate the funds needed to meet your lifestyle goals. Maybe your dream is to travel the world, which necessitates a larger budget, or perhaps you intend to lead a simple life, growing a garden at your countryside home, which requires less.

Recognizing and integrating these goals into your retirement budget ensures your financial strategy aligns with your envisioned lifestyle. This alignment is crucial for crafting a comprehensive 'budgeting for retirement' plan, setting you toward a fulfilling retirement.

Understand Your Income Streams

Retirement often signals a shift from a singular source of income to several. Understanding these varied income streams is integral to crafting a robust 'budgeting for retirement' plan. Let's dive deeper into this financial pool.

Social Security is a foundational income source for most retirees. The amount you receive depends on your work history, and it's crucial to know when and how to claim it to maximize benefits. Next, pensions, although less common now, provide a steady income flow for some retirees.

Retirement savings accounts, like 401(k)s and IRAs, are other substantial sources of retirement income. How you withdraw from these accounts can significantly affect their longevity and tax implications. Furthermore, passive income from investments, rental properties, or part-time work can supplement these primary income sources and add financial stability.

Lastly, annuities can be part of your retirement income strategy, providing a guaranteed income stream for a certain period or life.

Understanding and optimizing these diverse income streams are critical steps in your 'budgeting for retirement' journey, ensuring a more comfortable and secure retirement.

Outline Your Post-Retirement Expenses

Retiring does not mean the end of expenses. While some costs might decrease, like commuting or work clothes, others could increase, like health care or recreational activities. Therefore, estimating your retirement expenses realistically is crucial when 'budgeting for retirement.' Consider both fixed expenses (like housing and utilities) and variable costs (like travel or hobbies). Factor in inflation and unexpected expenses to ensure a more accurate and resilient budget.

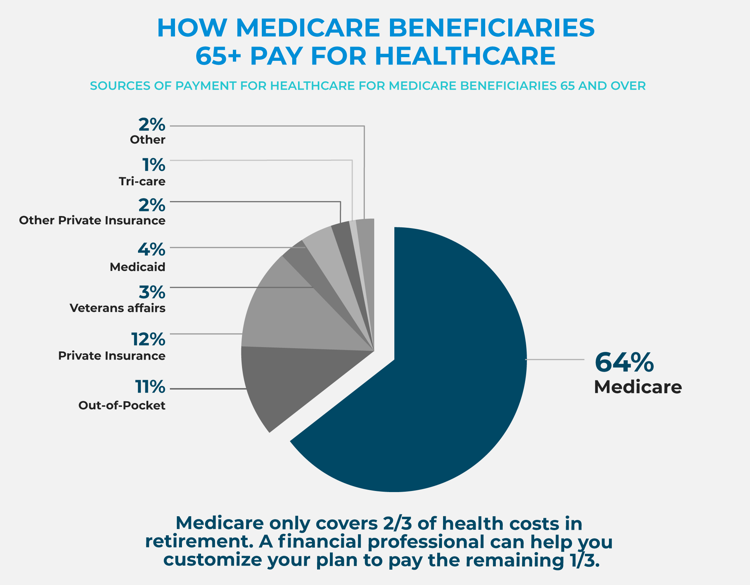

Credit: https://www.pacificlife.com/insights-articles/planning-for-the-cost-of-healthcare-in-retirement.html

Plan for Healthcare Costs

When crafting your retirement budget, allocating sufficient funds for potential healthcare costs is not just an option. It's a necessity. As we age, the likelihood of needing medical services increases, making healthcare a significant expense. Therefore, a comprehensive 'budgeting for retirement' strategy includes foreseeing these costs.

Your strategy should account for insurance premiums, which could come from Medicare or private insurance. Furthermore, you must factor in out-of-pocket costs for things not covered by insurance, such as deductibles, co-pays, and other unexpected medical expenses. With age, prescription medications are often needed more frequently.

Long-term care, including home care or assisted living, is another expense that could emerge in later life. While it's not pleasant to think about, planning for it financially can ease potential stress.

Finally, remember healthcare costs often rise faster than general inflation. Thus, your 'budgeting for retirement' plan should accommodate these increases to help ensure a secure and comfortable retirement.

Manage Your Debts

Debt management should be a key component of your retirement budget. Retirement savings shouldn't be used to pay off lingering debts during your golden years. So, what's the plan?

Firstly, understand the landscape of your debts. This means knowing who and how much you owe, including the interest rates and repayment terms. This analysis is a pivotal part of 'budgeting for retirement' as it sets the stage for an effective debt reduction strategy.

High-interest debts like credit card bills should be prioritized, given their potentially destructive nature on your finances. Paying off these debts before retirement can significantly enhance your financial security and free up more of your income for enjoyable retirement activities.

The approach might be different for more substantial and long-term debts, like mortgages or student loans. You may choose to continue payments into retirement or aim to eliminate these before retiring. The strategy should be individualized based on your financial situation and retirement goals.

Lastly, avoid accumulating new unnecessary debt as retirement approaches. Every new debt commitment can directly impact your 'budgeting for retirement plans, potentially delaying your retirement or diminishing its quality. Being conscious of your spending habits and maintaining sound financial discipline can be critical in managing your debts effectively.

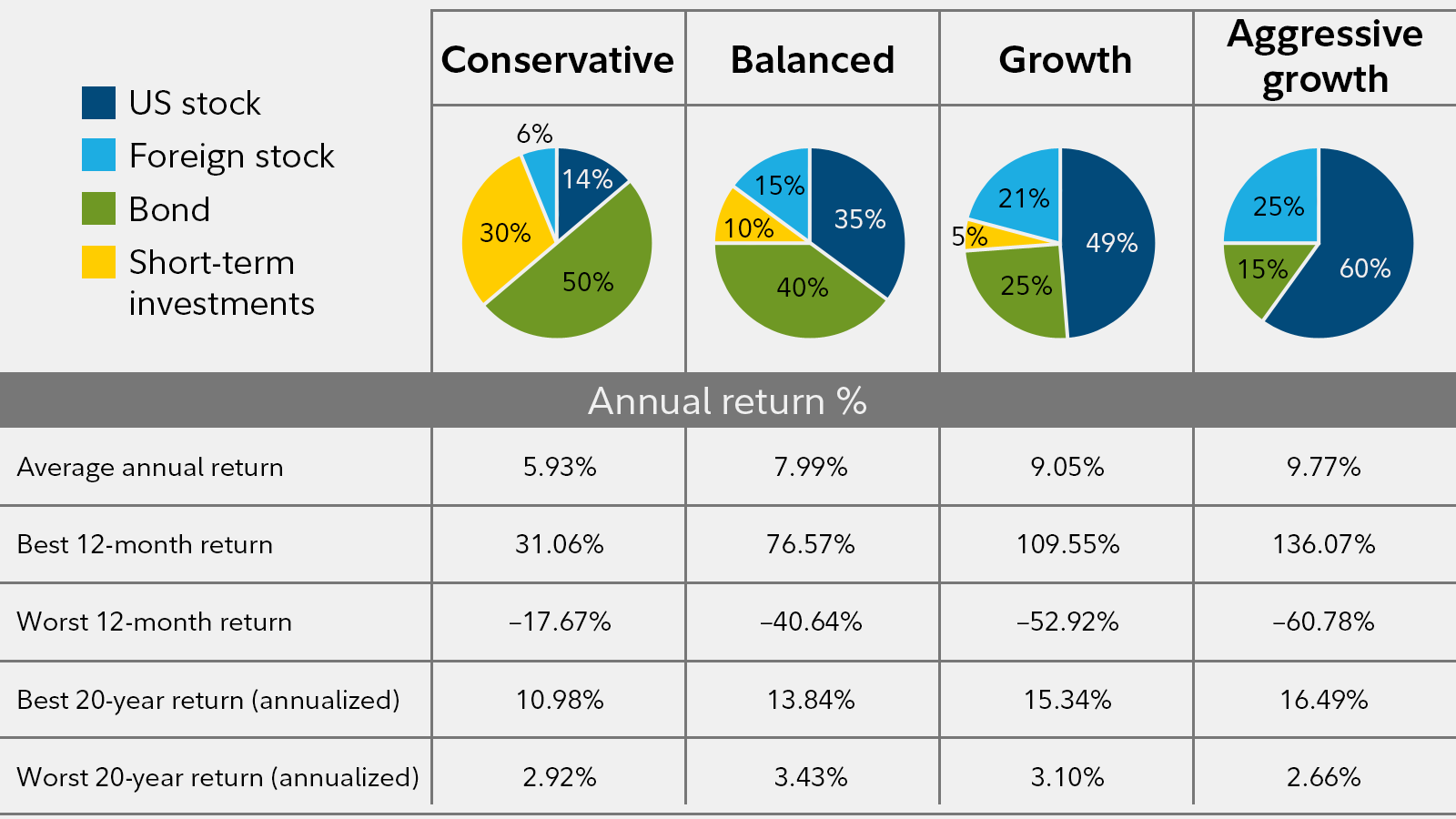

Maximize Your Savings and Investments

Budgeting for retirement requires efficient savings and investment management. The key is to save smarter, not just more. Contributing to retirement accounts is the first step in 401(k)s and Individual Retirement Accounts (IRAs). Tax advantages can boost your savings over time, helping you grow your savings faster. Within the law's limits, maximize these contributions.

Diversification of investments is another critical aspect. Invest in a variety of things rather than relying on one. Diversify your portfolio across assets, sectors, and regions to reduce the risk while potentially increasing the return. Always align your investment strategy with your risk tolerance and retirement timeline.

Lastly, consider compounding interest – the snowball effect where your earnings generate even more revenues over time. By starting early and investing wisely, your 'retirement budgeting' plan can become a growth engine that ensures financial comfort in your golden years.

Credit: https://www.fidelity.com/learning-center/investment-products/mutual-funds/diversification

Review and Adjust Your Plan Regularly

'Budgeting for retirement' is not a one-and-done event. As life changes, so too should your retirement plan. Major life events like marriage, children, home purchases, or career changes can impact your retirement plans. Regularly reviewing and adjusting your budget ensures it aligns with your goals and resources. Working with a financial advisor or using online retirement planning tools is often beneficial to help keep your retirement budget on track.

To sum up

In conclusion, effectively 'budgeting for retirement' is a multi-faceted process that involves careful planning and execution. From envisioning your retirement lifestyle to understanding income streams, estimating post-retirement expenses, preparing for healthcare costs, managing debts, and maximizing your savings and investments, each step plays a pivotal role in ensuring a secure future. Remember, your retirement budget is not set in stone and should be reviewed and adjusted periodically to align with life's changes. With these strategies, your retirement years can be as financially comfortable and fulfilling as the decades of hard work paved the way. It's never too early or late to start your journey toward a well-budgeted retirement.